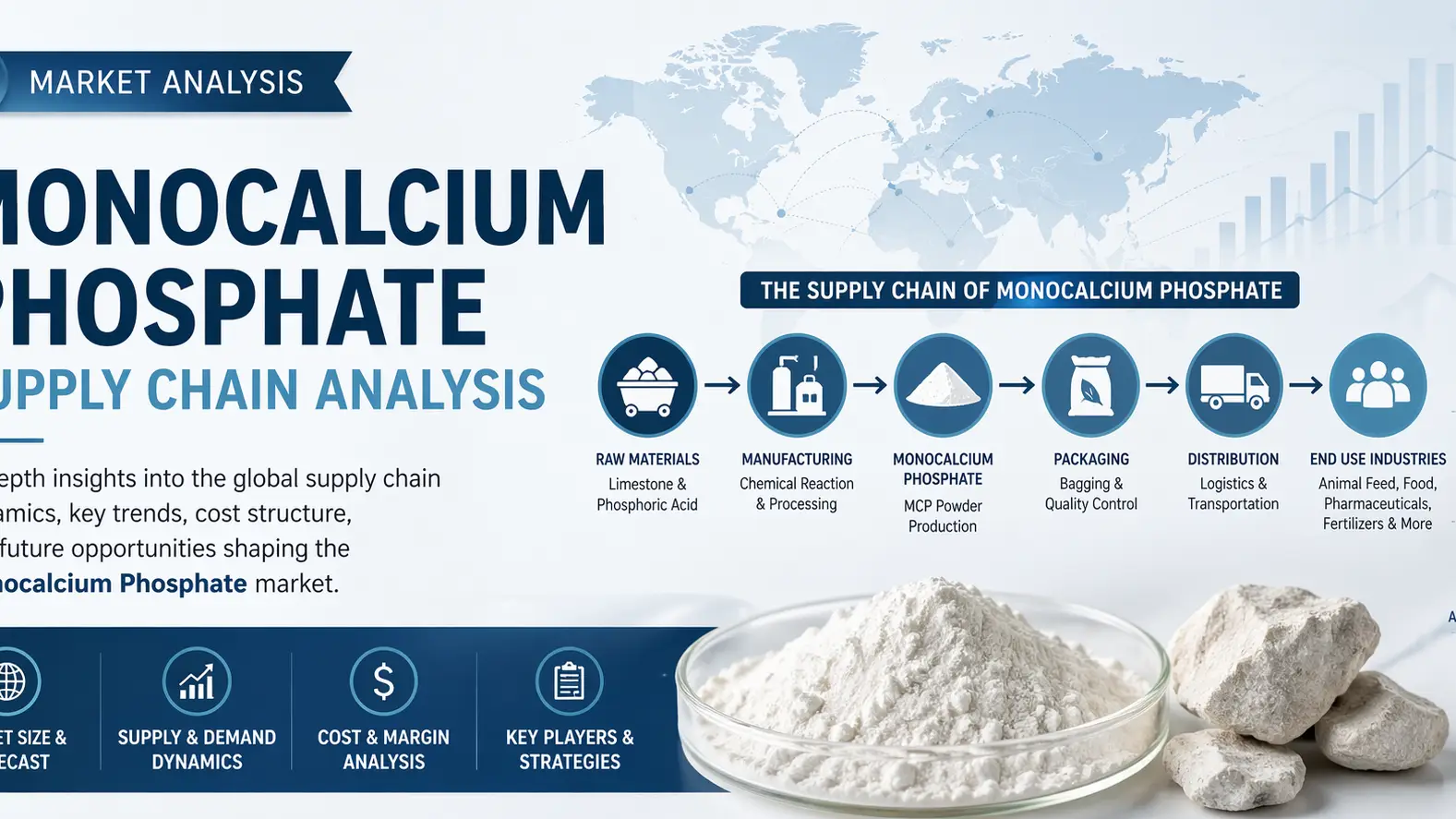

Introduction

Monocalcium phosphate (MCP) continues to establish itself as a critical platform chemical in global agriculture and animal nutrition value chains. As of 2026, its supply chain is shaped by tightening raw material availability, energy-intensive processing, and expanding demand from feed-grade applications. With global market expansion tracking a CAGR of 5.2%, MCP production has reached nearly 2.1 million MT annually, reflecting its strategic importance in phosphorus-based industrial systems. Pricing remains elevated within a band of USD 950–1,250/MT, driven by feedstock volatility and logistics constraints.

Phosphate Rock Sourcing Constraints and Geopolitical Control

The upstream supply chain begins with phosphate rock, where a limited number of countries dominate extraction. Morocco, China, and the United States collectively control over 70% of exportable reserves, creating structural dependency risks. In 2026, tightening environmental regulations and export quotas have reduced flexible supply availability by nearly 8–10%, directly influencing MCP cost stability and long-term contract pricing strategies.

Chemical Processing and Manufacturing Bottlenecks

MCP production relies on the acidulation of phosphate rock using phosphoric acid, a process highly sensitive to sulfur and energy input costs. Industrial facilities are increasingly centralized, with large-scale plants accounting for over 60% of global output. However, operational bottlenecks persist due to acid supply constraints and aging processing infrastructure in key Asian production hubs, limiting output scalability during peak agricultural demand cycles.

Global Logistics, Pricing Volatility, and Trade Routes

The MCP supply chain is heavily exposed to maritime freight fluctuations, particularly across Asia–Europe and Latin America corridors. In 2026, freight volatility has added up to 12–15% cost variability in landed prices. Export dependency from Southeast Asia has intensified, while import-heavy regions such as Europe face extended lead times. These disruptions reinforce the importance of diversified sourcing strategies and regional stockpiling.

Downstream Demand from Feed and Fertilizer Industries

Animal feed remains the dominant consumption segment, accounting for nearly 65% of global MCP demand. Expanding livestock production in Asia-Pacific and Latin America continues to drive consumption growth, supported by a rising focus on phosphate-balanced nutrition. Fertilizer applications also contribute to demand stability, particularly in soil nutrient recovery programs across developing agricultural economies.

Conclusion

Looking ahead, MCP’s supply chain will remain tightly interlinked with phosphate rock geopolitics, energy pricing, and agricultural demand cycles. Strategic resilience will depend on integrated sourcing, optimized logistics, and long-term supplier partnerships. In this evolving landscape, Tradeasia International stands out as a global chemical solution provider, offering dependable sourcing channels, streamlined distribution networks, and tailored supply chain support for industrial buyers navigating phosphate-based markets.

Sources

-

https://www.usgs.gov/centers/national-minerals-information-center/phosphate-rock-statistics-and-information

-

https://www.imarcgroup.com/monocalcium-phosphate-market

-

https://www.grandviewresearch.com/industry-analysis/monocalcium-phosphate-market

Leave a Comment