Millet Supply Chain Market Analysis 2026: Building Resilient Grain Networks

Introduction

Millet has evolved from a traditional staple grain into a strategically important agricultural commodity within the global food and feed industry. As climate adaptation, food security, and gluten-free nutrition continue shaping procurement strategies, millet is increasingly positioned as a platform agricultural ingredient for diversified food manufacturing and industrial applications. In 2026, the global millet market is benefiting from expanding demand across Asia-Pacific, Africa, Europe, and North America, supported by rising health awareness and government-backed sustainable farming programs.

The market is projected to grow at a CAGR of 5.8% between 2026 and 2031, while global millet production is estimated to exceed 42 million metric tons in 2026. The strengthening supply chain ecosystem—from cultivation and aggregation to processing and export distribution—is becoming a decisive factor influencing pricing stability, quality assurance, and long-term commercial scalability.

Expanding Millet Production and Global Trade Dynamics

India remains the dominant producer in the global millet supply chain, contributing nearly 40% of total world production, followed by key suppliers including Nigeria, Niger, China, and Sudan. Favorable drought resistance and lower water dependency continue driving millet cultivation in semi-arid agricultural regions where climate volatility is disrupting conventional cereal farming.

International trade volumes are also expanding steadily, particularly for pearl millet and finger millet varieties used in flour, breakfast cereals, snacks, and health-focused packaged foods. Export-oriented supply chains are strengthening in response to growing procurement demand from Europe and the Middle East, where importers are seeking traceable, sustainably sourced grains with stable nutritional profiles.

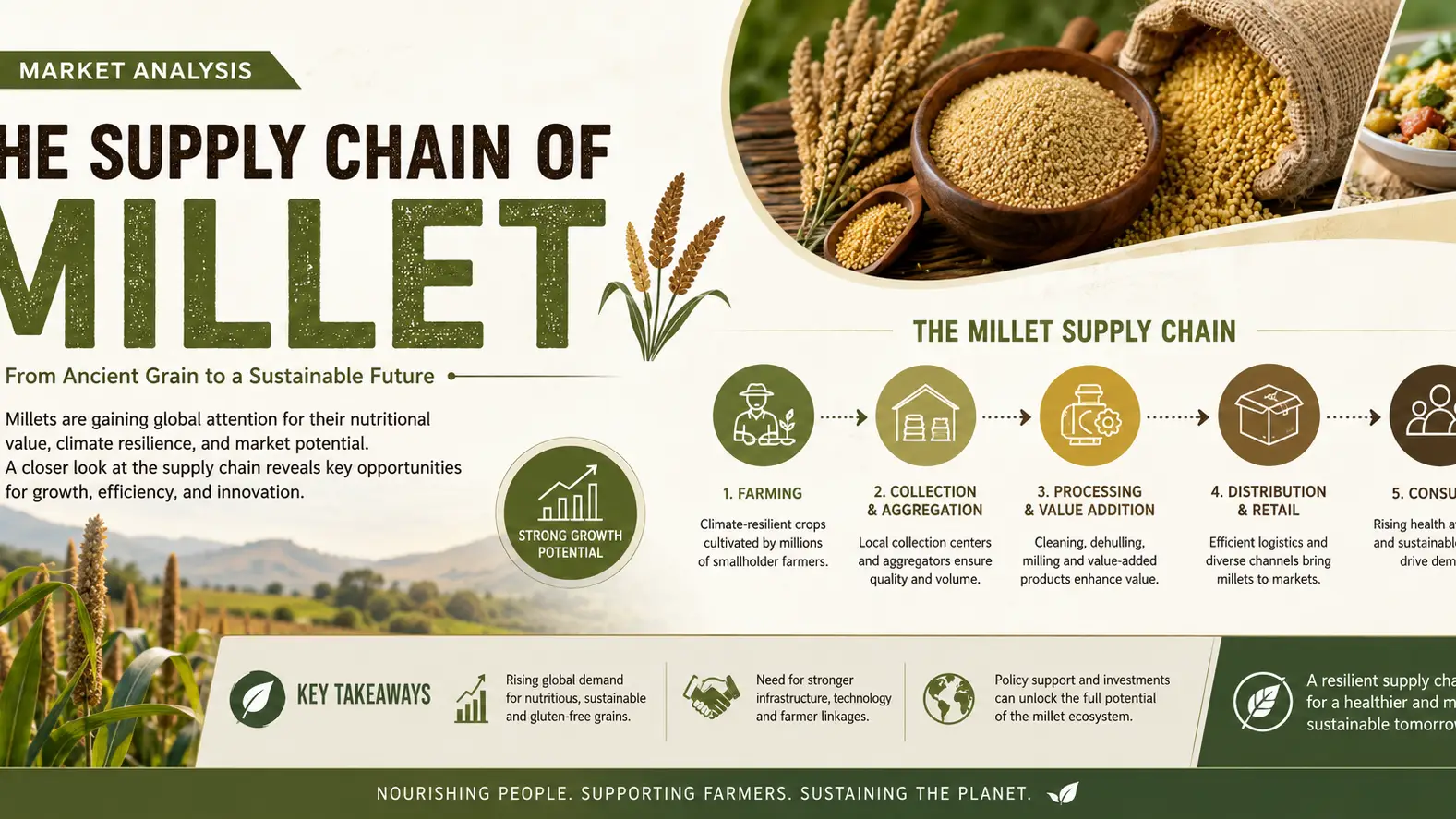

Processing Infrastructure and Value-Added Opportunities

The modernization of millet processing infrastructure is becoming a central growth catalyst for the industry. Investment in automated cleaning, dehulling, grading, and milling facilities is improving product consistency while reducing post-harvest losses across developing producer economies.

In 2026, processed millet products account for nearly 55% of commercial trade value, reflecting rising demand for ready-to-use ingredients and fortified grain blends. Food manufacturers are increasingly integrating millet into bakery products, dairy alternatives, energy bars, and functional beverages. This shift is encouraging supply chain participants to prioritize integrated sourcing partnerships and regional storage facilities that can support large-volume industrial buyers.

Pricing Trends and Supply Chain Cost Pressures

Millet pricing remains relatively competitive compared to wheat and corn, although supply chain disruptions and transportation costs continue affecting regional procurement patterns. Average export prices for bulk millet in 2026 range between USD 280–420/MT, depending on origin, grain quality, and processing level.

Freight inflation, storage inefficiencies, and inconsistent harvesting infrastructure in certain producing regions remain significant operational concerns. However, long-term procurement contracts and localized aggregation hubs are helping stabilize supply availability for multinational food processors and commodity traders.

Growing digitalization within agricultural logistics is also improving shipment visibility and inventory forecasting, enabling buyers to reduce sourcing risks while enhancing supply chain responsiveness.

Sustainability, Procurement, and Future Distribution Models

Sustainability has become a major competitive advantage in the millet market. Compared to conventional cereals, millet requires significantly less irrigation and demonstrates stronger resilience under extreme weather conditions. As a result, institutional buyers and food brands are increasingly integrating millet into ESG-driven sourcing frameworks.

Governments and agricultural agencies are supporting millet commercialization through farmer training programs, subsidy incentives, and export promotion initiatives. These policies are expected to strengthen regional distribution networks and improve long-term market accessibility, particularly in emerging economies.

The next phase of supply chain development will likely focus on traceability systems, climate-smart farming partnerships, and expanded processing capacity designed to support premium-grade export demand.

Conclusion

As a platform agricultural commodity, millet is steadily transitioning from a traditional grain into a globally traded ingredient with expanding industrial and commercial relevance. The 2026 supply chain landscape reflects stronger integration between producers, processors, exporters, and food manufacturers seeking sustainable and resilient sourcing solutions.

For companies navigating global millet procurement, Tradeasia International offers reliable supply chain support through international sourcing networks, quality-focused distribution, and tailored commodity trading solutions designed to meet evolving market demands across the food and agricultural sectors.

Sources

Leave a Comment