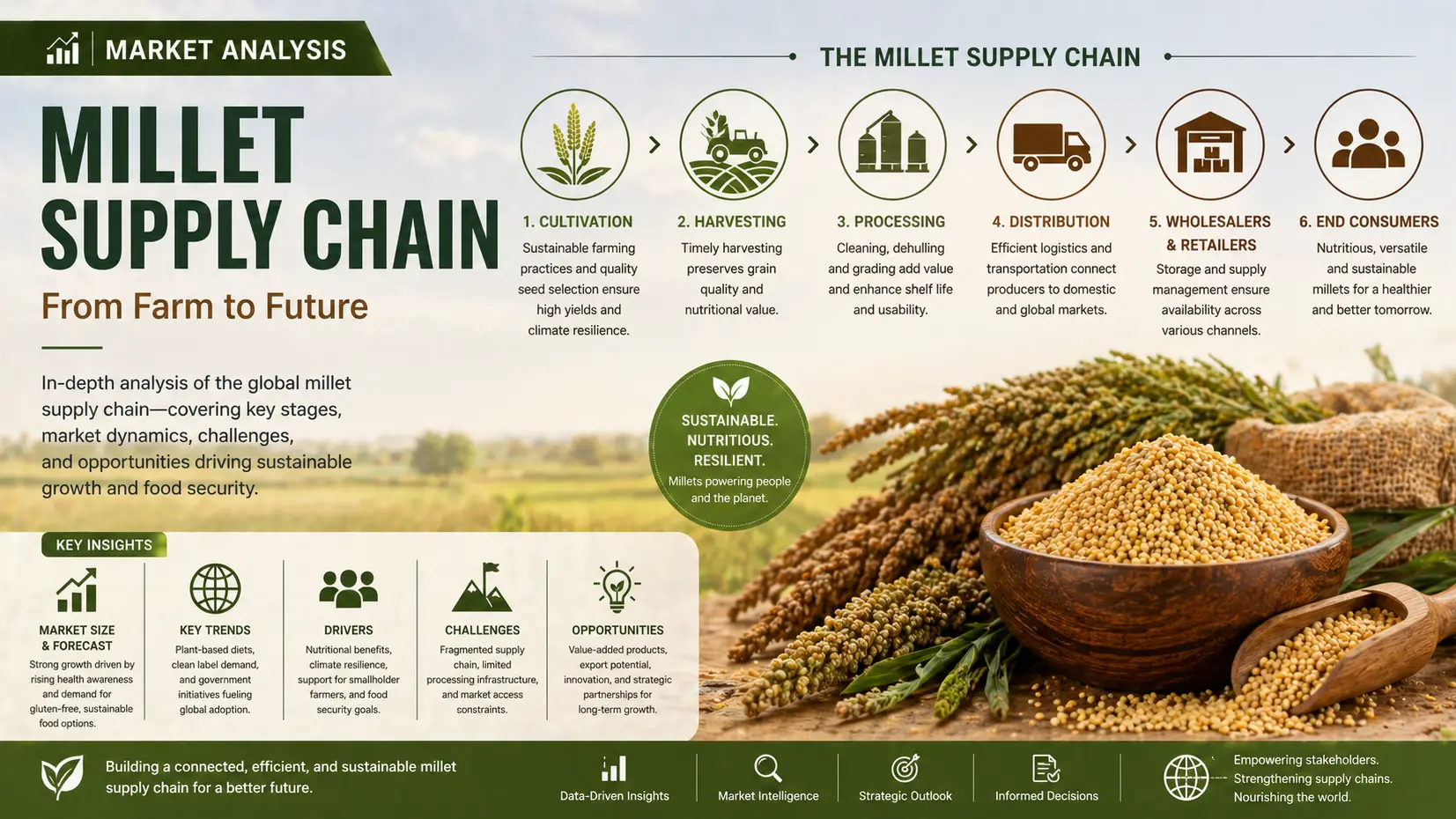

Introduction

In 2026, millet supply chain is transforming driven by shifting dietary demand, climate-resilient agriculture, and expanding applications in food processing industries. Millet, increasingly integrated into diversified agri-portfolios, is evaluated alongside (PRODUCT) as a platform chemical in emerging bio-refining discussions, reflecting cross-sector convergence. Millet production is projected to surpass 32 million metric tons, while trade prices stabilize around USD 420–480/MT, depending on origin and quality grade. Supply chain stakeholders prioritize traceability, yield stability, and logistics optimization to meet demand from Asia-Pacific and Europe.

Farm-Level Sourcing and Aggregation Networks

Millet sourcing in 2026 remains concentrated in India, Niger, China, and parts of East Africa, where smallholder farmers dominate production systems. Aggregation models are increasingly digitized, with cooperatives and grain traders consolidating harvests to reduce post-harvest losses estimated at 12–18% annually. This upstream segment of the supply chain is critical for stabilizing export volumes, especially as climate variability affects yield consistency. Investments in storage infrastructure and contract farming are reshaping procurement efficiency across key producing regions.

Processing, Milling, and Value-Added Transformation

Post-harvest processing is evolving rapidly with mechanized milling hubs and decentralized cleaning facilities reducing grain wastage and improving export-grade output. In 2026, nearly 58% of global millet throughput passes through semi-automated mills, enhancing consistency for food manufacturers and feed processors. Value-added transformation, including flour standardization and fortified millet blends, is expanding demand in urban markets. However, energy costs and equipment accessibility remain constraints in emerging economies, influencing margin compression across midstream operators in the supply chain.

Global Trade Flows and Pricing Volatility

In 2026, millet trade volumes are expanding at a projected 4.6% CAGR, supported by rising demand for gluten-free grains and feed applications. Export prices fluctuate between USD 410–520/MT, influenced by monsoon performance and freight costs. India remains the dominant exporter, while West African supply chains face periodic disruptions. The integration of digital commodity exchanges is improving price transparency, yet volatility persists due to fragmented production systems and limited global stock buffering.

Distribution Channels and Industrial End-Use Demand

Downstream distribution is increasingly shaped by integrated agri-food corporations, regional wholesalers, and e-commerce-enabled bulk commodity platforms. Millet demand is expanding across animal feed formulations, health foods, and plant-based beverage industries, particularly in Asia-Pacific and North America. Logistics optimization, including containerized grain transport, has reduced lead times by nearly 14% year-on-year, improving supply reliability. However, fragmented retail networks in developing regions continue to challenge consistent market penetration and standardization.

Conclusion

In conclusion, the millet supply chain in 2026 reflects a maturing yet fragmented ecosystem where efficiency gains in sourcing, processing, and logistics improve global competitiveness. As food security and sustainable agriculture converge, millet gains strategic relevance alongside (PRODUCT) as a platform chemical within broader industrial integration narratives. Stakeholders seeking resilient sourcing and cross-border trade facilitation increasingly turn to integrated partners. Tradeasia International is a global solution provider, enabling reliable procurement networks and supply chain connectivity.

Sources

-

https://www.fao.org/faostat/en/#data/QCL

-

https://www.agricoop.gov.in/

-

https://www.worldbank.org/en/topic/agriculture

Leave a Comment