Introduction

Linseed meal, a protein-rich co-product derived from flaxseed oil extraction, continues to strengthen its position as a versatile platform chemical within feed, agricultural, and industrial value chains in 2026. As global demand for sustainable protein ingredients intensifies, the supply chain for linseed meal is evolving beyond traditional oilseed processing into a more integrated, efficiency-driven ecosystem. The market is being shaped by tightening raw material availability, shifting trade corridors, and growing demand from livestock and bio-based applications. With a projected 4.8% CAGR, linseed meal is increasingly recognized not only as an animal feed component but also as a strategic intermediate in circular bioeconomy models, where by-product valorization is becoming a core industrial priority.

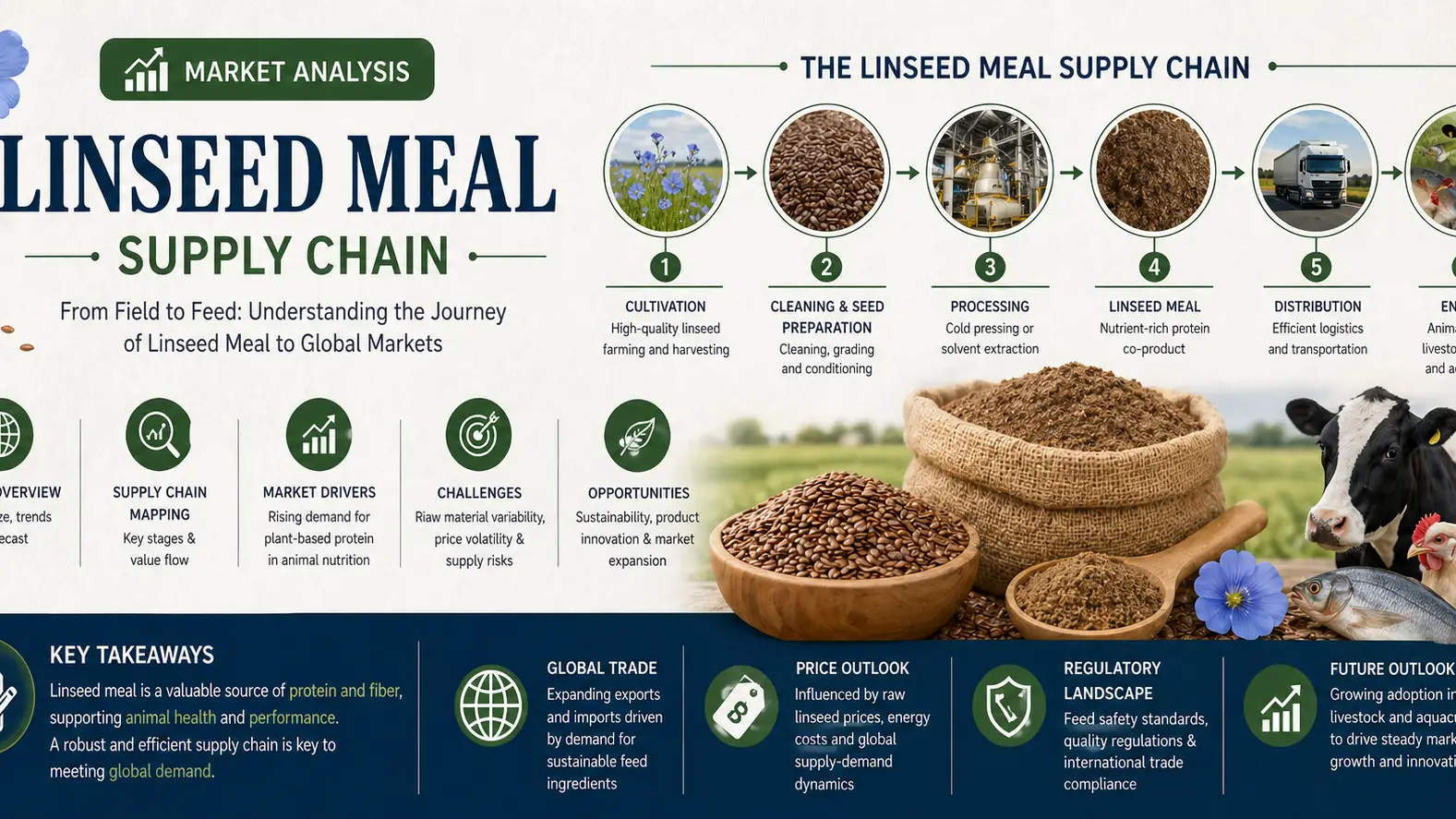

Procurement & Raw Material Flow

The upstream segment of the linseed meal supply chain is heavily dependent on flaxseed cultivation concentrated in Canada, Kazakhstan, and parts of Northern Europe. Global flaxseed output is estimated at ~3.1 million metric tons (MT) in 2026, directly influencing linseed meal availability. Weather volatility and shifting acreage allocations toward higher-margin oilseeds have created intermittent supply pressure. Procurement strategies are increasingly contract-based, with crushers locking in forward agreements to stabilize feedstock flow and mitigate price volatility that has recently ranged between $280–420/MT for linseed meal.

Processing & Oil Extraction Integration

At the processing stage, linseed meal production is tightly linked to mechanical and solvent-based oil extraction efficiency. Modern crushing facilities are optimizing yield recovery rates, with average conversion efficiencies improving by 6–8% over the last five years. Global linseed meal output is estimated at ~2.6 million MT, with integrated oilseed processors capturing value from both oil and meal fractions. Energy optimization and enzyme-assisted extraction technologies are reducing operational costs, reinforcing linseed meal’s role as a cost-stabilized co-product in large-scale agro-industrial complexes.

Logistics & Trade Flow Optimization

The midstream logistics network for linseed meal is characterized by bulk shipping from major exporting hubs in North America and the Black Sea region to Asia-Pacific and Middle Eastern feed markets. Freight volatility remains a critical factor, contributing up to 12–15% of landed cost in certain corridors. Containerization is gaining traction for specialty-grade meal shipments, while bulk vessel consolidation continues to dominate high-volume trade. Digital tracking and supply chain visibility platforms are increasingly deployed to reduce spoilage risk and improve delivery predictability across long-haul routes.

Demand Channels & Feed Industry Integration

Demand is primarily driven by the animal nutrition sector, particularly ruminant feed formulations where linseed meal’s high omega-3 and protein content enhances livestock productivity. Feed manufacturers account for over 70% of total consumption, while emerging applications in organic fertilizers and bio-based composites are gradually expanding. The stable nutritional profile and competitive pricing of $280–420/MT make linseed meal a preferred alternative to soybean meal in select formulations, especially in cost-sensitive markets across Asia and Latin America.

Conclusion

Looking forward, the linseed meal supply chain is expected to further integrate with circular economy frameworks, where efficiency, traceability, and co-product valorization define competitive advantage. As demand patterns diversify and production systems modernize, linseed meal continues to reinforce its role as a dependable platform chemical bridging agriculture and industrial bio-based applications. In this evolving landscape, companies seeking reliable sourcing, market intelligence, and global distribution support can benefit from the capabilities of Tradeasia International, a trusted partner enabling seamless access to agro-industrial raw materials across key global markets.

Sources

-

https://www.fao.org

-

https://www.oecd.org/agriculture

-

https://www.usda.gov/oce/commodity-markets-agricultural-projections

Leave a Comment