Global L-Valine Supply Chain Transformation: From Fermentation to End-Use Integration

Introduction: L-Valine as a Strategic Biochemical in Modern Industrial Supply Chains

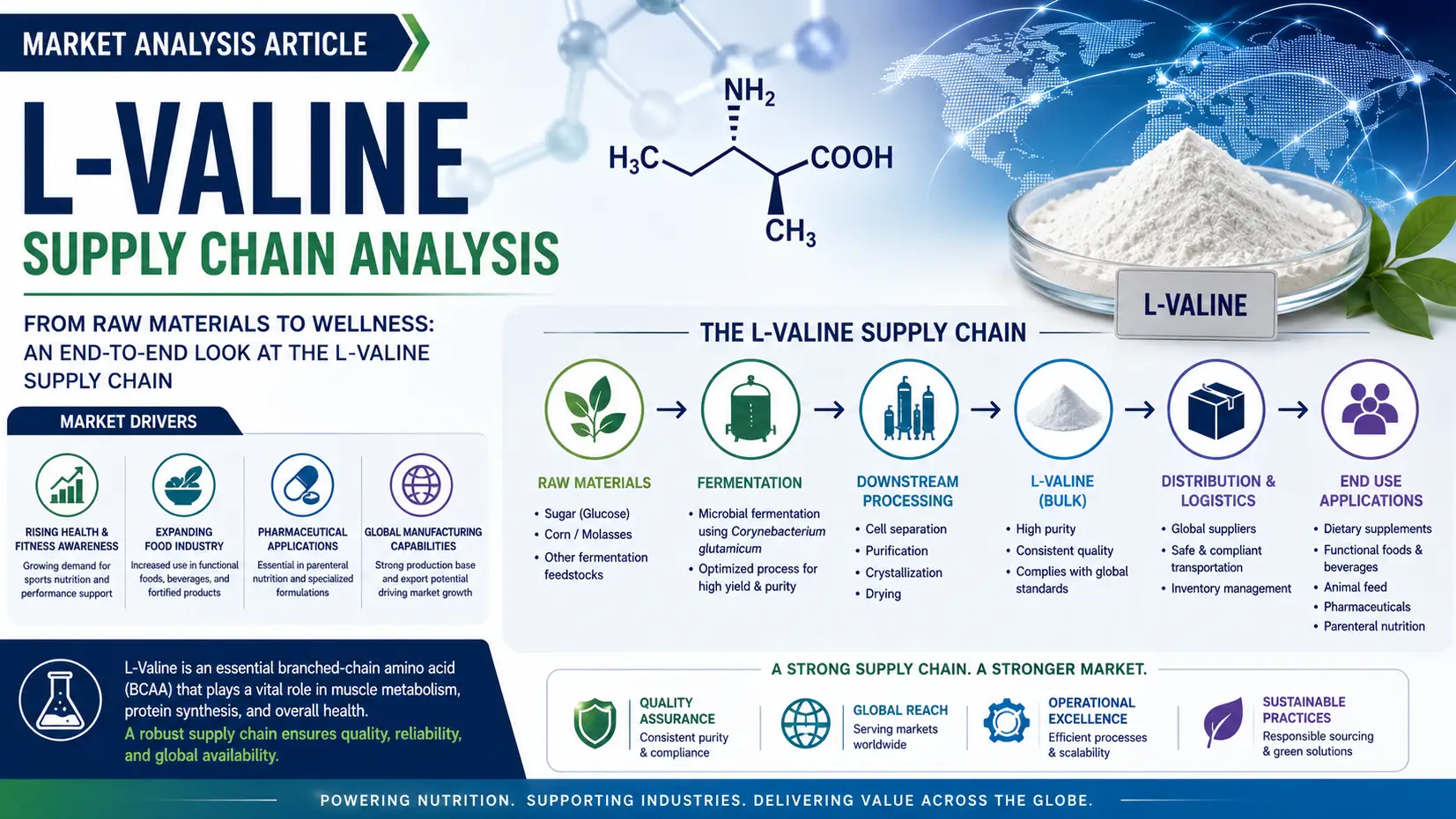

L-valine, a key branched-chain amino acid, continues to strengthen its position as a strategic platform chemical in 2026, driven by expanding applications in animal nutrition, pharmaceuticals, and biotech fermentation systems. The L-valine supply chain is increasingly shaped by bio-based production efficiency, regional manufacturing clusters, and volatile feedstock costs. With global demand growing at a projected CAGR of 5.4%, the market is steadily transitioning from fragmented sourcing to vertically integrated production ecosystems, while average pricing stabilizes between USD 6,800–8,400/MT depending on purity grade and contract scale.

Fermentation Feedstock Economics and Raw Material Stability

The upstream segment of the L-valine supply chain is dominated by glucose, corn steep liquor, and other carbohydrate-rich inputs. Feedstock costs account for nearly 55–62% of total production expenses, making price volatility a core risk factor. In 2026, corn-derived glucose prices have stabilized, supporting fermentation efficiency improvements of nearly 8–10% year-on-year yield gains. However, energy-linked costs still influence overall pricing dynamics, especially in export-oriented production zones.

Asia-Pacific Production Concentration and Capacity Expansion

Asia-Pacific remains the global hub, accounting for over 72% of total L-valine production, led by China and emerging Indian biotech manufacturers. Global output is estimated at approximately 85,000 MT in 2026, with new fermentation capacity expansions adding nearly 6,000–8,000 MT annually. This concentration improves cost competitiveness but also increases exposure to regional regulatory and environmental compliance pressures, reshaping global sourcing strategies.

Logistics Optimization and Global Trade Flow Disruptions

The L-valine supply chain is increasingly sensitive to maritime freight fluctuations and container imbalances. While amino acids do not require cold-chain handling, purity preservation and moisture control remain critical during transit. Freight normalization in 2026 has reduced logistics costs by nearly 12% from 2024 peaks, yet lead times remain unstable for Europe-bound shipments. Strategic warehousing in free-trade zones is becoming a preferred buffer against geopolitical and shipping volatility.

Demand Structure and Downstream Market Integration

Downstream demand is primarily driven by animal feed formulations, accounting for nearly 68% of global consumption, followed by pharmaceutical and nutraceutical applications. The integration of L-valine into precision livestock nutrition continues to accelerate, particularly in poultry and swine feed optimization. This demand stability supports long-term contract pricing mechanisms, reducing spot market exposure and reinforcing supplier-buyer partnerships across global value chains.

Conclusion

As L-valine strengthens its role as a high-value platform chemical, supply chain resilience is becoming a defining competitive factor. Producers are increasingly focusing on integrated fermentation systems, diversified sourcing, and regional distribution hubs to manage cost and risk volatility. In this evolving landscape, global buyers are prioritizing partners with end-to-end supply reliability and technical support capabilities. Tradeasia International stands as a strategic enabler in this ecosystem, offering seamless chemical sourcing solutions, stable supply networks, and cross-regional distribution expertise to support industrial buyers navigating the complexities of the 2026 L-valine market.

Sources

Leave a Comment