Introduction

The guar meal market in 2026 continues to strengthen its position as a vital agri-derived byproduct within the global feed and bio-based ingredient ecosystem. Derived from guar seed processing, guar meal is increasingly recognized not only as a high-protein livestock feed component but also as a flexible platform ingredient supporting sustainable protein substitution strategies. With global production volumes reaching approximately 1.4 million MT and a steady expansion trajectory, the market is advancing at a projected 5.2% CAGR. Price movements remain moderately volatile, ranging between USD 350–520/MT, shaped by agricultural yields, export demand, and processing capacity constraints.

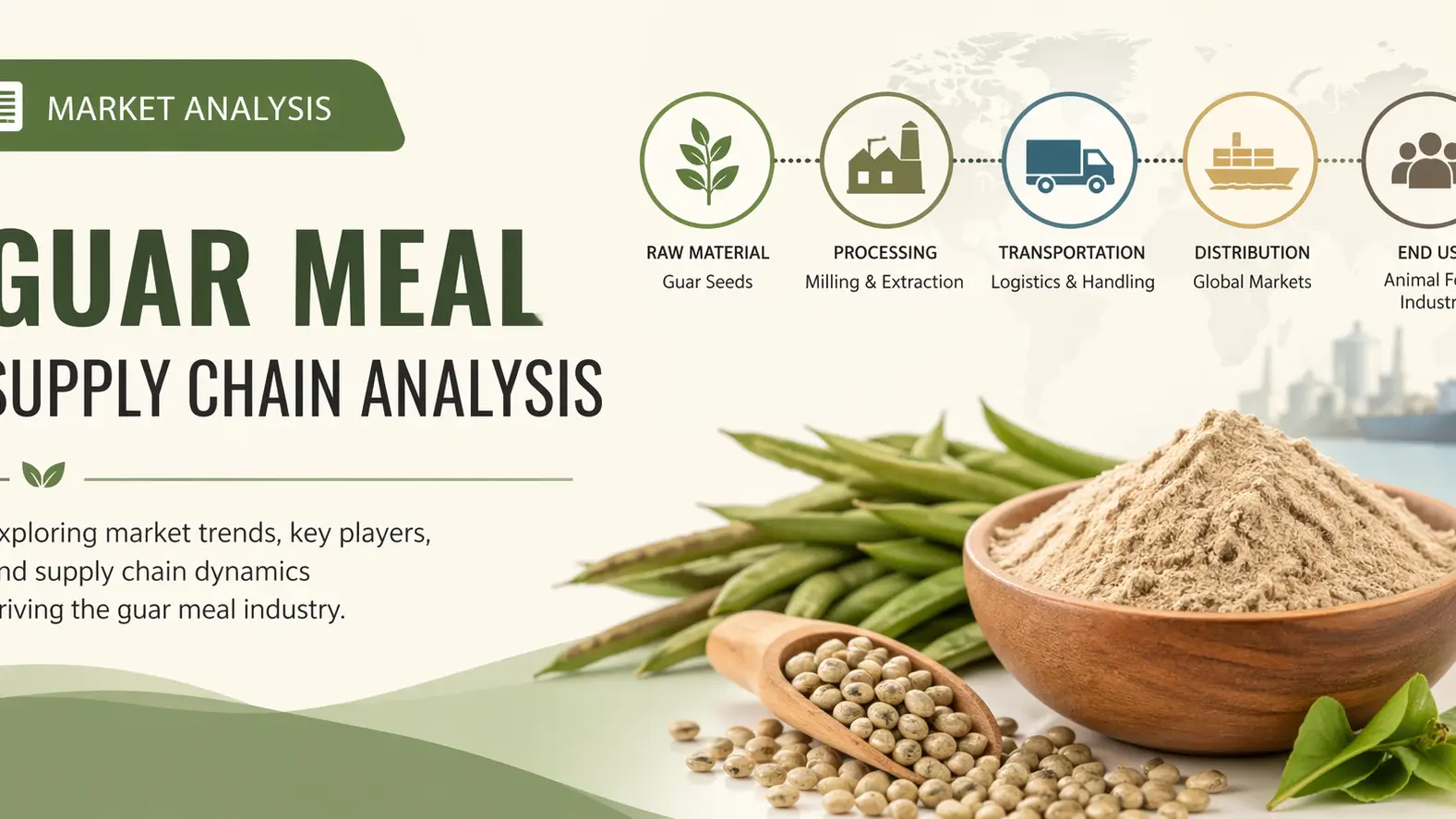

Raw Material Sourcing and Agricultural Dependence

The guar meal supply chain begins in arid agricultural belts, primarily India and Pakistan, where guar seed cultivation is highly dependent on monsoon performance and irrigation efficiency. India alone contributes over 80% of global guar seed output, making its agronomic cycles central to supply stability. Seasonal fluctuations directly impact crushing volumes, with seed availability influencing downstream meal production consistency. In 2026, raw material tightening in Rajasthan and Gujarat has introduced periodic price firmness, reinforcing guar meal’s sensitivity to climatic and soil productivity risks.

Processing Infrastructure and Value Conversion

Guar meal is produced through mechanical dehusking and splitting of guar seeds in specialized crushing mills. These facilities generate guar gum as the primary product while producing meal as a high-protein byproduct containing 45–50% crude protein. Processing efficiency and energy optimization remain key cost drivers, especially as operational expenses increase across South Asian milling hubs. Industrial upgrading has improved throughput, yet fragmented small-scale processors continue to create uneven quality grades within export markets.

Global Logistics and Trade Flow Dynamics

The export-oriented nature of guar meal supply chains places logistics at the center of market competitiveness. Major outbound shipments move through Indian ports such as Mundra and Kandla, targeting livestock feed markets in Europe, the Middle East, and Southeast Asia. Freight volatility and container availability have introduced periodic supply delays, while compliance with feed safety standards has added documentation complexity. Trade flows remain highly responsive to soybean meal price differentials, reinforcing guar meal’s role as a cost-adjustable protein alternative.

Demand Structure and Feed Industry Integration

Demand for guar meal is primarily anchored in poultry and cattle feed formulations, where it serves as a cost-effective protein substitute. Its integration into compound feed systems is expanding as feed manufacturers seek diversification away from soybean dependency. Growing livestock consumption is supporting long-term demand expansion aligned with the 5.2% CAGR outlook. Buyers are increasingly prioritizing consistent protein profiles and traceable sourcing, reshaping procurement strategies across feed producers and integrators.

Conclusion

As guar meal continues to evolve as a resilient agri-commodity, its positioning as a bio-based feed ingredient underscores its broader role as a platform chemical within sustainable agricultural value chains. Supply chain efficiency, from farm-level sourcing to export logistics, will define competitiveness in the coming years. In this evolving landscape, companies like Tradeasia International play a strategic role by connecting global buyers with reliable guar meal supply networks, ensuring consistent quality, pricing stability, and streamlined procurement solutions across markets.

Sources

-

https://www.feedipedia.org/node/311 (Feedipedia)

-

https://pmc.ncbi.nlm.nih.gov/articles/PMC10838761/ (PMC)

-

https://www.sciencedirect.com/science/article/pii/S0032579119432549 (sciencedirect.com)

Leave a Comment