Global Fish Solubles Supply Chain Transformation 2026

Introduction: Fish Solubles as Platform Chemical

Fish solubles, a nutrient-dense liquid derived from fishmeal and seafood processing residues, are increasingly positioned as a platform chemical within the circular bioeconomy. In 2026, the market reflects a tightening balance between sustainability mandates and rising global demand from aquafeed and agricultural sectors. The industry is estimated to expand at a CAGR of 4.8%, supported by improved recovery efficiency and integrated marine processing systems. However, supply chain resilience remains a defining challenge, as feedstock variability and regulatory constraints directly influence output consistency and pricing stability across global trade routes.

Supply Chain Structure and Primary Flows

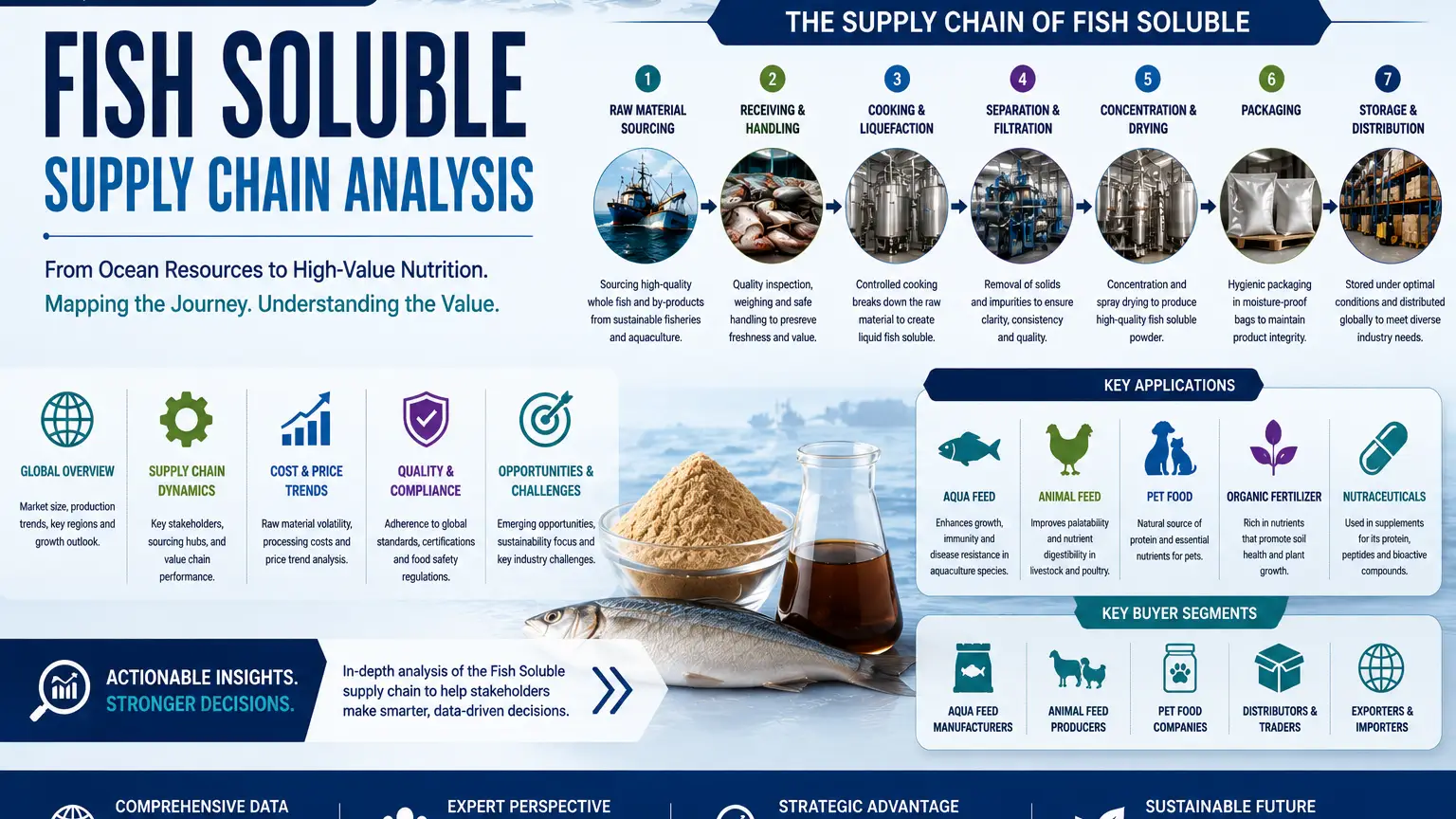

The fish solubles supply chain begins at marine capture fisheries and aquaculture processing plants, where by-products are rendered into liquid hydrolysates. Global production reaches approximately 1.2 million MT in 2026, with major output concentrated in Peru, Norway, and Southeast Asia. These regions dominate export flows due to advanced processing infrastructure and integrated coastal logistics. Midstream operations include stabilization, filtration, and concentration, while downstream blending hubs distribute material to feed and fertilizer manufacturers across fragmented international markets.

Raw Material Sourcing and Cost Pressures

Raw material sourcing is highly sensitive to seasonal catch variability, quota restrictions, and fuel-driven fishing costs. Input pricing fluctuates between USD 180–320/MT, depending on protein concentration and processing grade. Latin America and the EU are strengthening waste utilization regulations, improving raw material availability but not fully eliminating volatility. As a result, long-term procurement contracts and vertical integration strategies are increasingly adopted to secure consistent supply and reduce exposure to upstream disruptions.

Processing, Storage, and Logistics Optimization

Fish solubles require rapid stabilization immediately after extraction to prevent microbial degradation, making processing speed a critical supply chain determinant. Investments in enzymatic preservation and controlled storage have reduced spoilage losses by nearly 15% in modern facilities. Export logistics rely on ISO tank containers and bulk liquid shipping systems, with transit lead times ranging from 10–25 days depending on destination and port congestion. These logistics efficiencies are central to maintaining product integrity and global competitiveness.

Demand Dynamics and Market Integration

Global demand for fish solubles is expanding steadily, particularly in aquafeed formulations and organic fertilizer production. The market is forecast to grow at a CAGR of 5.1%, driven by rising sustainable agriculture adoption and protein efficiency requirements. Asia-Pacific accounts for over 45% of total consumption, while Europe focuses on high-value bio-based applications and circular economy integration. This demand shift is reinforcing the product’s strategic role within renewable bio-industrial supply chains.

Conclusion

Fish solubles continue to evolve as a strategic platform chemical linking marine resource efficiency with high-value industrial applications. As global supply chains mature, integration across processing, logistics, and end-use industries becomes essential for maintaining both cost competitiveness and sustainability compliance. In this evolving landscape, Tradeasia International stands as a reliable global solution provider, enabling secure sourcing, streamlined distribution, and consistent industrial-grade supply for feed and fertilizer manufacturers worldwide.

Sources

Leave a Comment