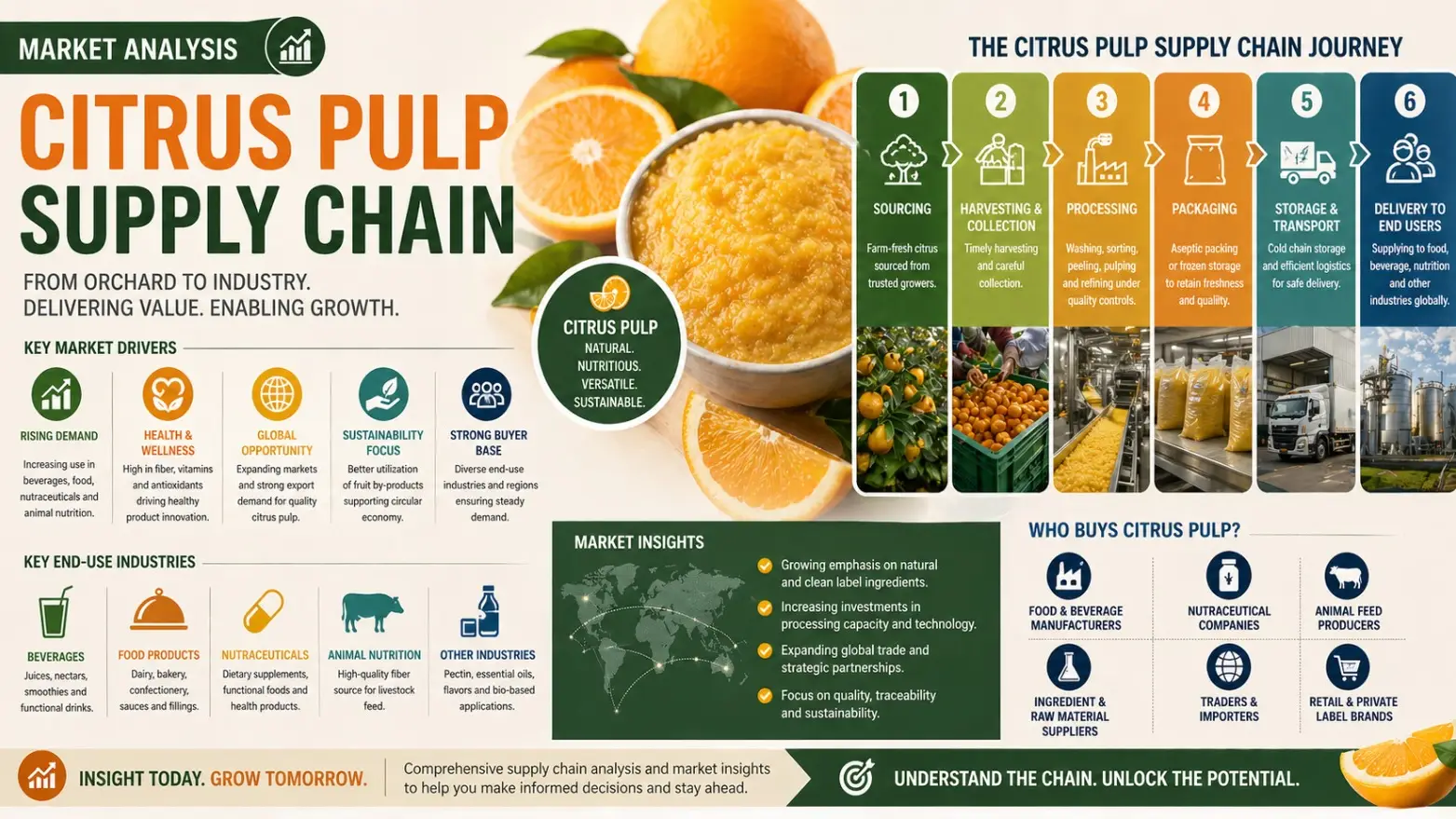

Global Citrus Pulp Supply Chain Dynamics and Market Developments 2026

Introduction: Citrus Pulp Emerging as a Strategic Industrial Feedstock

Citrus pulp has evolved from a low-value agro-industrial residue into a commercially strategic platform chemical within the global feed and bio-based ingredient economy. Derived primarily from orange, lemon, and grapefruit processing, citrus pulp is increasingly utilized in ruminant feed formulations, pectin extraction, bioenergy generation, and organic fertilizer production. By 2026, the global citrus pulp supply chain market is estimated to surpass 41 million metric tonsin annual production volume, supported by expanding citrus processing activities in Brazil, Mexico, Spain, and the United States. Market analysts project a compound annual growth rate (CAGR) of 5.8% between 2024 and 2029 as livestock producers seek cost-efficient and fiber-rich feed alternatives.

Brazil and Mediterranean Processing Capacity Expansion

Brazil continues to dominate the citrus pulp supply chain, accounting for nearly 65% of global dried citrus pulp exports in 2026. Major orange juice processors are scaling integrated waste recovery systems to maximize pulp utilization efficiency. Meanwhile, Spain and Turkey are strengthening Mediterranean supply capabilities through investments in dehydration technology and pelletization facilities. Export-grade citrus pulp pellet prices have stabilized between USD 210–290/MT depending on moisture content and freight conditions. Increased automation across processing hubs has also reduced operational losses by approximately 12%, improving global supply reliability.

Feed Industry Demand Reshaping Global Trade Routes

The global feed sector remains the primary demand driver for citrus pulp. Rising corn and soybean meal prices have encouraged feed manufacturers to incorporate citrus pulp as a digestible fiber substitute for cattle and dairy operations. In Asia-Pacific, particularly China and South Korea, imports of citrus pulp pellets increased by over 18% year-on-year entering 2026. This shift has intensified bulk commodity movements from South America toward East Asian ports, altering traditional Atlantic-focused trade patterns. Simultaneously, Middle Eastern feed integrators are securing long-term citrus pulp contracts to stabilize procurement costs amid volatile grain markets.

Freight Volatility and Citrus Waste Valorization Economics

Supply chain profitability in 2026 remains heavily influenced by freight fluctuations and energy costs. Ocean freight rates for agricultural dry bulk cargoes experienced periodic spikes exceeding 22% during peak harvest quarters, directly affecting landed citrus pulp prices. However, processors are offsetting logistics pressure through circular economy strategies. Citrus waste streams are increasingly converted into biogas, essential oils, and industrial pectin derivatives, creating diversified revenue channels. These value-added applications are helping processors maintain competitive margins even during periods of lower feed commodity demand.

Sustainability Pressures Accelerating Supply Chain Innovation

Environmental compliance has become central to citrus pulp market competitiveness. Large beverage and juice manufacturers are implementing zero-waste processing initiatives to meet carbon reduction commitments and ESG targets. Advanced drying systems with lower thermal energy consumption are reducing processing emissions by nearly 15% across modern facilities. Buyers are also prioritizing traceable sourcing and certified sustainable supply chains, especially in European markets where regulatory scrutiny surrounding agricultural byproducts continues to intensify.

Conclusion

As a platform chemical and feed industry ingredient, citrus pulp is steadily transitioning into a high-value component of the global agricultural supply chain. The combination of rising livestock feed demand, waste valorization technologies, and sustainability-driven processing investments is expected to sustain long-term market expansion beyond 2026. Companies capable of ensuring stable sourcing, efficient logistics, and consistent product quality will remain strategically positioned within this evolving sector.

In this increasingly interconnected market environment, Tradeasia International continues to support global industries with reliable sourcing networks, integrated supply chain solutions, and extensive expertise in agricultural and industrial raw materials, helping businesses navigate changing commodity dynamics with greater operational confidence.

Sources

Leave a Comment