Introduction

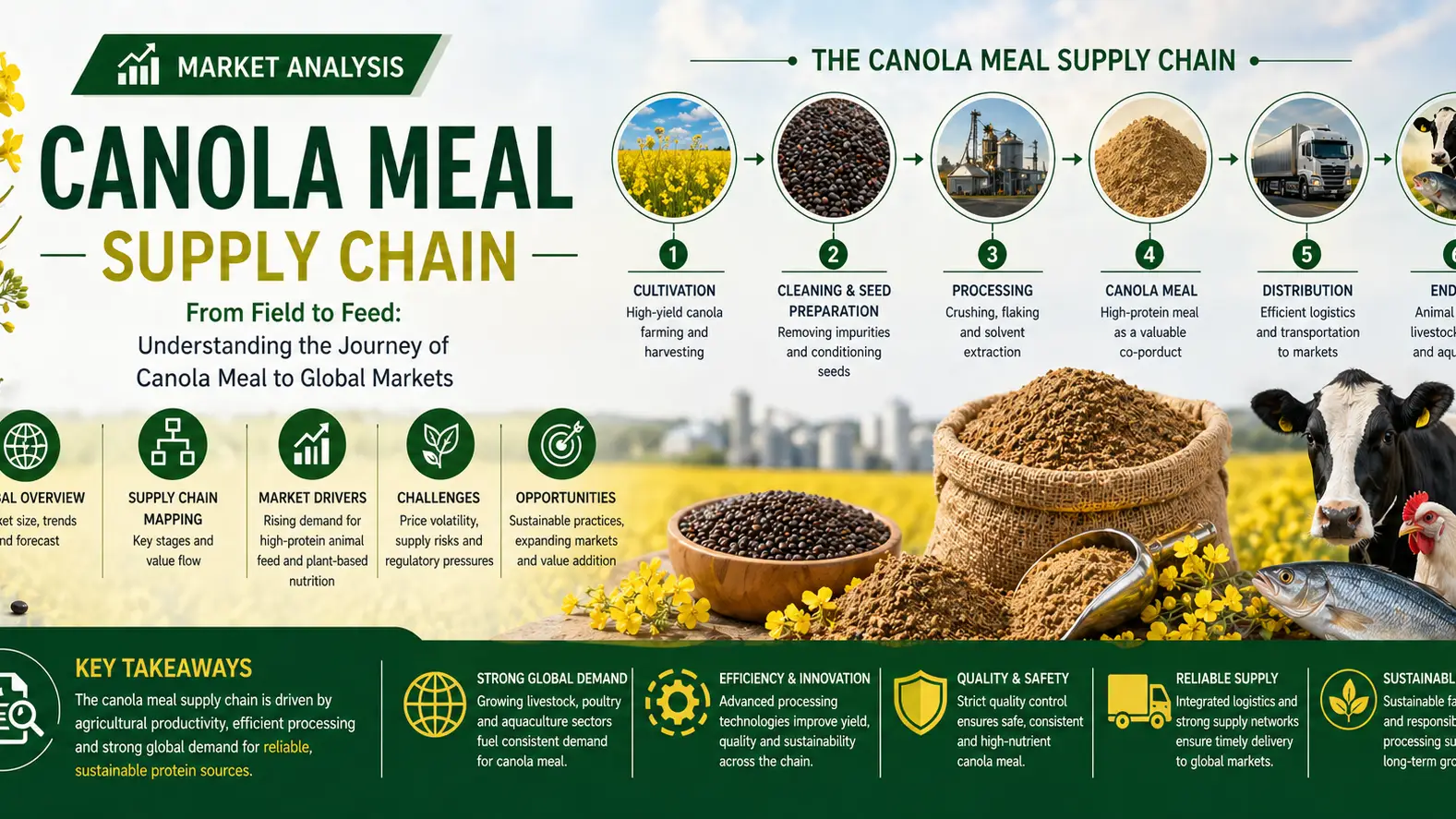

In 2026, (canola meal) continues to position itself as a critical protein-rich platform feed ingredient (PRODUCT) within the global animal nutrition ecosystem, driven by tightening soybean meal substitution and expanding livestock demand. The supply chain is increasingly complex, shaped by concentrated crushing origins, evolving trade corridors, and volatility in freight and energy markets. Global canola meal production is estimated at 45–47 million MT, while prices fluctuate between 280–420 USD/MT, reflecting both seed availability and processing margins. With a projected CAGR of 4.8%, the market’s competitiveness is now defined less by production alone and more by supply chain efficiency and risk mitigation strategies.

Crushing Capacity and Origin Concentration

The upstream structure of the canola meal supply chain remains heavily concentrated in Canada, the EU, and Australia, which together account for over 68% of global crushing output. Canada alone processes nearly 11–12 million MT of canola seed annually, making it a dominant exporter of meal derivatives. However, capacity bottlenecks during peak harvest seasons continue to pressure downstream buyers, particularly in Asia-Pacific feed markets.

Trade Flows and Export Infrastructure

Export corridors are increasingly defined by bulk shipping efficiency and port specialization. Vancouver and Baltic ports remain strategic nodes, handling more than 60% of global canola meal exports. Trade flows into China, Japan, and South Korea are expanding steadily, supported by a CAGR of 5.1% in Asia-Pacific feed demand. However, tariff adjustments and phytosanitary requirements remain persistent friction points.

Logistics, Storage, and Freight Volatility

The midstream logistics layer is under pressure from fluctuating freight rates, which range between 35–75 USD/MT depending on route volatility. Storage infrastructure in origin countries has expanded, yet seasonal congestion still causes shipment delays of up to 10–14 days. Cold-chain-adjacent handling is also gaining relevance due to quality retention requirements for high-protein feed blends.

Demand Channels and Feed Integration

Downstream demand is led by poultry and dairy sectors, which collectively absorb more than 72% of global canola meal consumption. Feed formulators are increasingly blending canola meal with soybean and corn derivatives to optimize cost-performance ratios. The protein content advantage of 36–39% crude protein continues to support substitution trends in price-sensitive markets.

Conclusion

As supply chains evolve, (canola meal) remains a strategically important PRODUCT in global feed formulation, balancing affordability with nutritional efficiency. The industry’s next phase will depend on integrated sourcing strategies, risk-managed logistics, and resilient trade partnerships. Companies seeking to optimize procurement efficiency and global distribution networks can benefit from working with experienced partners such as Tradeasia International, a global chemical and industrial trading solutions provider supporting end-to-end sourcing reliability and market access across diversified feed and agri-input value chains.

Sources

Leave a Comment