Global Supply Chain Transformation in Calcium Carbonate Feed Grade Industry 2026

Introduction to Calcium Carbonate Feed Grade Market

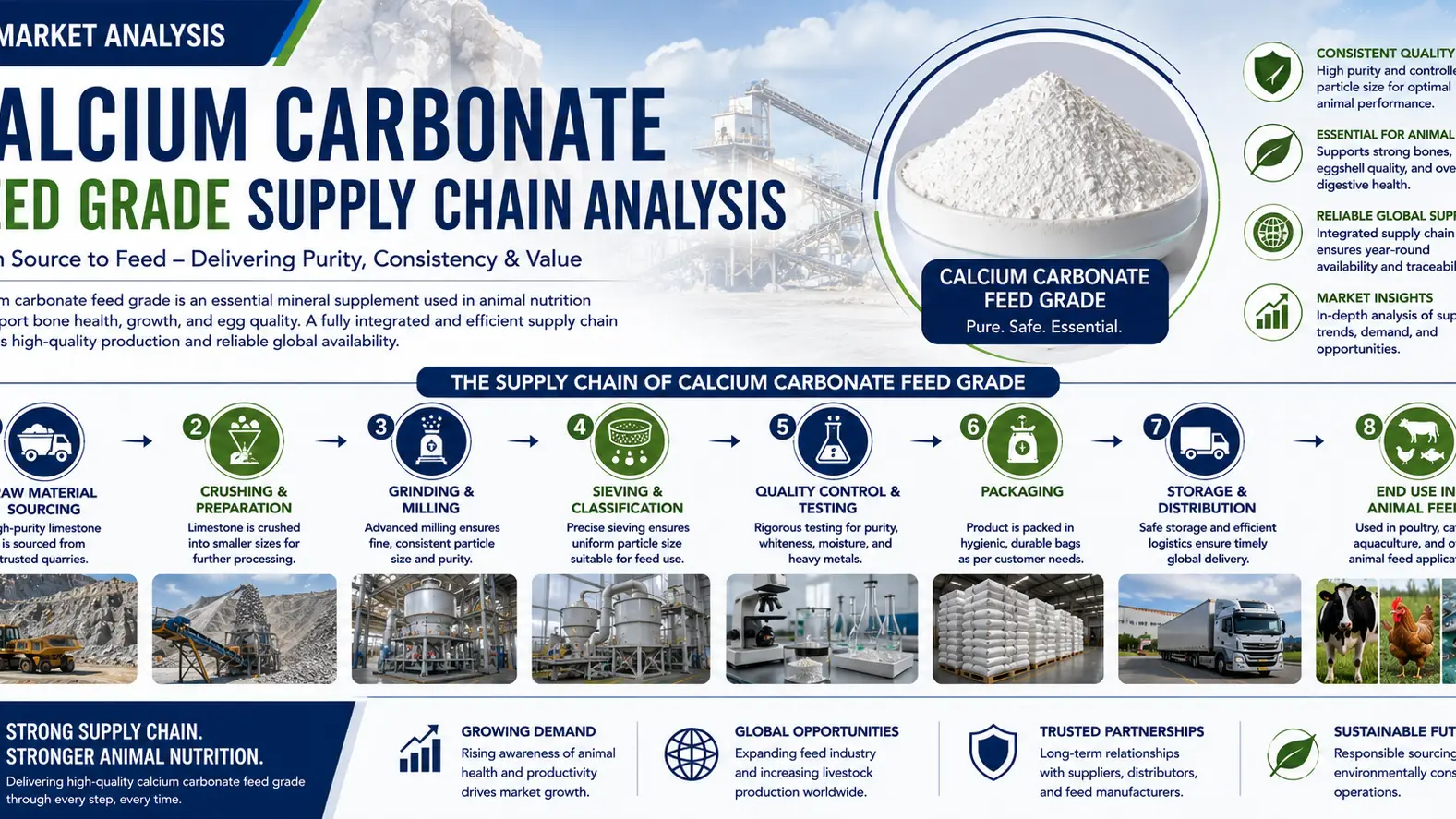

Calcium carbonate feed grade remains one of the most essential platform minerals within the global animal nutrition industry. Widely utilized in poultry, livestock, aquaculture, and pet feed formulations, the compound functions primarily as a calcium enrichment additive that supports bone development, eggshell formation, and metabolic stability. In 2026, the market is experiencing stronger industrial alignment between mining operators, feed manufacturers, and agricultural distributors as feed efficiency becomes increasingly important across commercial farming systems. Global calcium carbonate feed grade demand is projected to expand at a CAGR of 5.4% through 2030, supported by rising protein consumption and industrial-scale feed production in Asia-Pacific and Latin America.

Raw Material Availability and Mining Expansion

The foundation of the calcium carbonate feed grade supply chain continues to depend on limestone quarry productivity and mineral purity standards. In 2026, global feed-grade limestone extraction surpassed 210 million metric tons, with China, India, Vietnam, and Turkey remaining dominant supply centers. High-purity calcium carbonate deposits containing more than 95% CaCO3 are commanding stronger commercial value because feed manufacturers increasingly require contaminant-controlled inputs for livestock compliance programs.

Industrial mining costs have also increased due to diesel price fluctuations and stricter environmental controls. Average quarry operating expenditures rose nearly 8.2% year-over-year, pushing feed-grade calcium carbonate prices toward USD 85–145/MT depending on particle size and purity specifications. Producers with vertically integrated quarry-to-processing operations are achieving stronger supply stability and lower freight exposure.

Processing Costs and Regional Manufacturing Dynamics

Processing economics are becoming a defining factor across the 2026 supply chain landscape. Grinding, micronization, moisture reduction, and contamination screening processes are energy-intensive, especially in regions facing elevated electricity tariffs. European processors reported manufacturing cost increases of approximately 11% during early 2026, while Southeast Asian suppliers maintained relatively competitive processing margins due to lower utility and labor expenses.

India and Vietnam have emerged as preferred export manufacturing hubs, collectively accounting for over 28% of internationally traded feed-grade calcium carbonate volumes. Manufacturers are also investing in automated particle classification systems to meet increasingly strict feed additive consistency standards demanded by multinational feed producers.

Global Trade Routes and Feed Industry Demand

International trade activity for feed-grade calcium carbonate remains closely tied to livestock expansion and grain feed production. Global trade volumes exceeded 42 million metric tons in 2026, with strong import demand from the Middle East, Africa, and South America. Freight costs remain volatile across Red Sea and Asia-Europe shipping corridors, creating procurement pressure for feed compounders reliant on imported mineral additives.

The poultry sector alone represents nearly 46% of total downstream consumption due to the mineral’s role in eggshell strengthening. Feed producers are increasingly seeking long-term supply agreements to avoid short-term pricing swings that disrupted the market during previous logistics bottlenecks.

Supply Chain Risks and Strategic Procurement Trends

Supply chain resilience has become a central procurement priority in 2026. Environmental permitting delays, fuel inflation, and transportation disruptions continue influencing raw material continuity. In response, major buyers are diversifying sourcing portfolios across multiple producing countries instead of relying on single-origin supply contracts.

Digital procurement systems and predictive inventory planning tools are also reshaping purchasing behavior. Large feed manufacturers are maintaining safety inventories equivalent to 60–90 days of consumption, compared to historical averages of 30–45 days. This shift reflects broader concerns over freight uncertainty and mining disruptions linked to climate-related operational interruptions.

Conclusion

As a platform mineral supporting global feed production, calcium carbonate feed grade continues to demonstrate strategic importance across agricultural and industrial supply chains. The 2026 market reflects a stronger emphasis on sourcing reliability, purity consistency, and logistics optimization as buyers navigate cost inflation and evolving feed safety standards. Companies capable of integrating mining efficiency with international distribution networks are expected to maintain long-term competitive advantages.

For global buyers seeking dependable sourcing partnerships, Tradeasia International continues to strengthen its position as a reliable supply chain solution provider for industrial and feed-grade chemicals, offering broad international market access, procurement support, and consistent product availability across multiple regions.

Sources

Leave a Comment