Global Broken Rice Supply Chain Dynamics: Production, Trade, Logistics & Demand 2026

Introduction: Broken Rice Market 2026: From Milling By-Product to Strategic Global Commodity

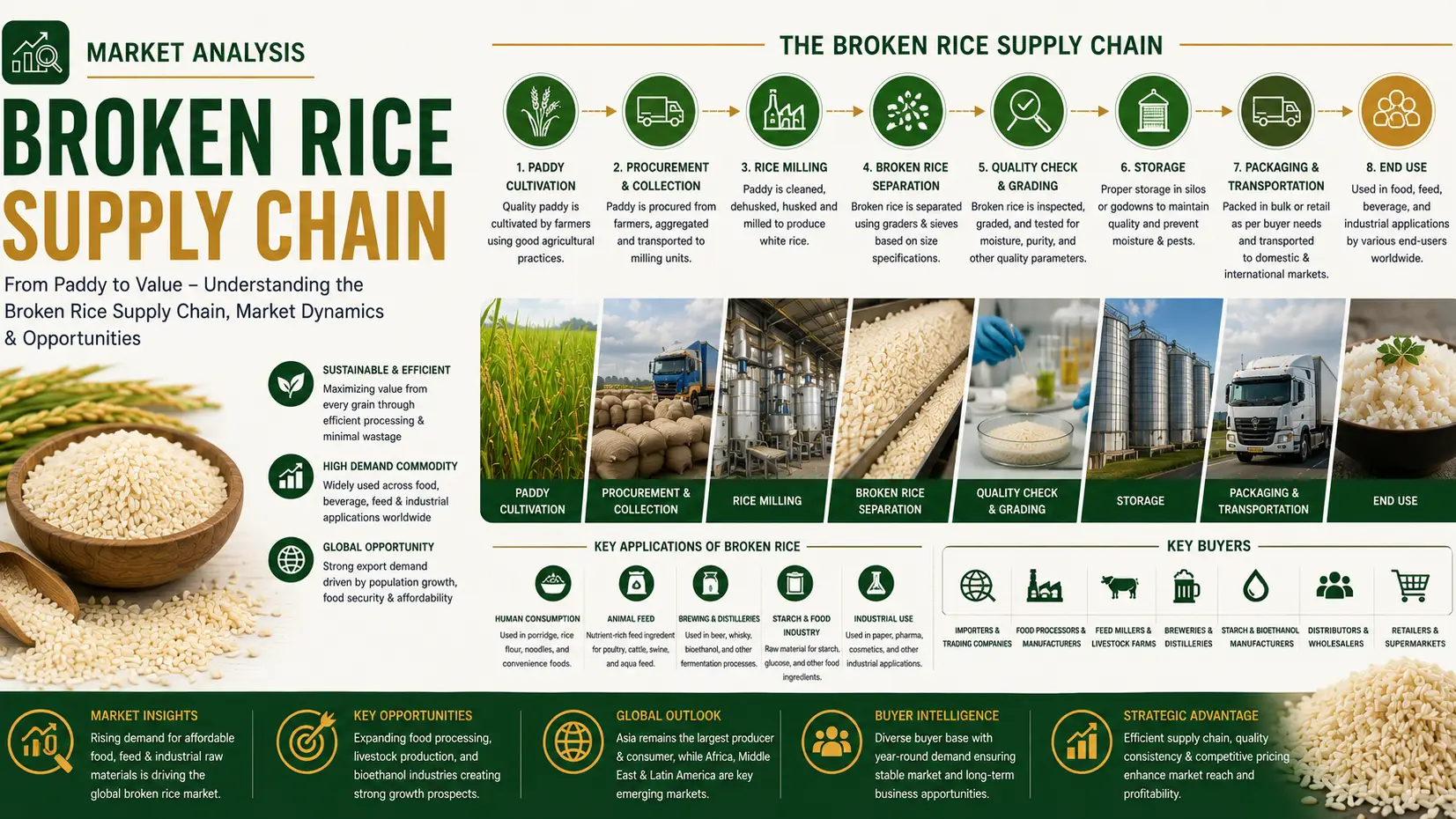

Broken rice, long considered a by-product of milling, has evolved into a strategically traded agro-commodity and a platform ingredient in food processing, ethanol blending, and animal feed systems. As of 2026, the global broken rice supply chain is shaped by tightening grain balances, rising bio-based demand, and shifting export policies across Asia. Global production is estimated at 38–42 million metric tons, derived from nearly 520 million metric tons of milled rice output, growing at a steady 3.9% CAGR. Prices remain structurally elevated, ranging between USD 185–320/MT, reflecting both freight pressures and demand diversification.

Milling Efficiency and Production Dynamics

Supply chain fundamentals begin at milling recovery rates, where modern rice mills in India and Vietnam achieve broken rice yields of 7–12% per ton of paddy. Efficiency upgrades in 2026 have slightly increased output volumes, but quality differentiation between whole grain and broken fractions continues to shape downstream pricing. Industrial-grade broken rice, particularly for fermentation, commands a premium due to its starch consistency.

Export Hubs and Trade Flow Concentration

Global trade remains highly concentrated, with India, Thailand, and Vietnam controlling over 68% of export volumes. India alone contributes nearly 12–15 million metric tons annually, benefiting from cost advantages and large-scale procurement systems. However, periodic export restrictions and policy interventions create volatility, forcing buyers in Africa and Southeast Asia to diversify sourcing strategies.

Logistics, Pricing Volatility, and Freight Constraints

Broken rice supply chains are heavily exposed to maritime freight fluctuations and port congestion across South and Southeast Asia. Container shortages and rising bunker fuel costs have added 8–12% logistics premiums to landed prices in 2026. This has widened regional arbitrage gaps, particularly between FOB Vietnam and CIF African markets, influencing procurement timing and contract structures.

Industrial Demand and End-Use Market Expansion

Demand is expanding beyond traditional feed applications, with growing use in starch extraction, brewing, and ethanol production. The industrial segment now accounts for nearly 35% of total global broken rice consumption, up from 28% in 2022. Feed manufacturers continue to anchor baseline demand due to its cost efficiency versus maize and wheat substitutes.

Conclusion

As global agro-commodity chains evolve, broken rice has transitioned from a milling residue into a strategically traded industrial input with diversified applications. Its pricing resilience and expanding industrial footprint underscore its importance in food security and bio-based manufacturing systems. In this context, efficient sourcing, consistent quality supply, and integrated logistics become critical for downstream users.

Companies such as Tradeasia International play a pivotal role in strengthening global access to agro-based raw materials, enabling buyers to secure consistent broken rice supply across multiple origins while optimizing cost and logistics efficiency in an increasingly volatile trade environment.

Sources

Leave a Comment