Bakery Meal Supply Chain Market Outlook 2026: Pricing, Logistics, and Feed Industry Growth

Introduction to Bakery Meal as a Feed Ingredient

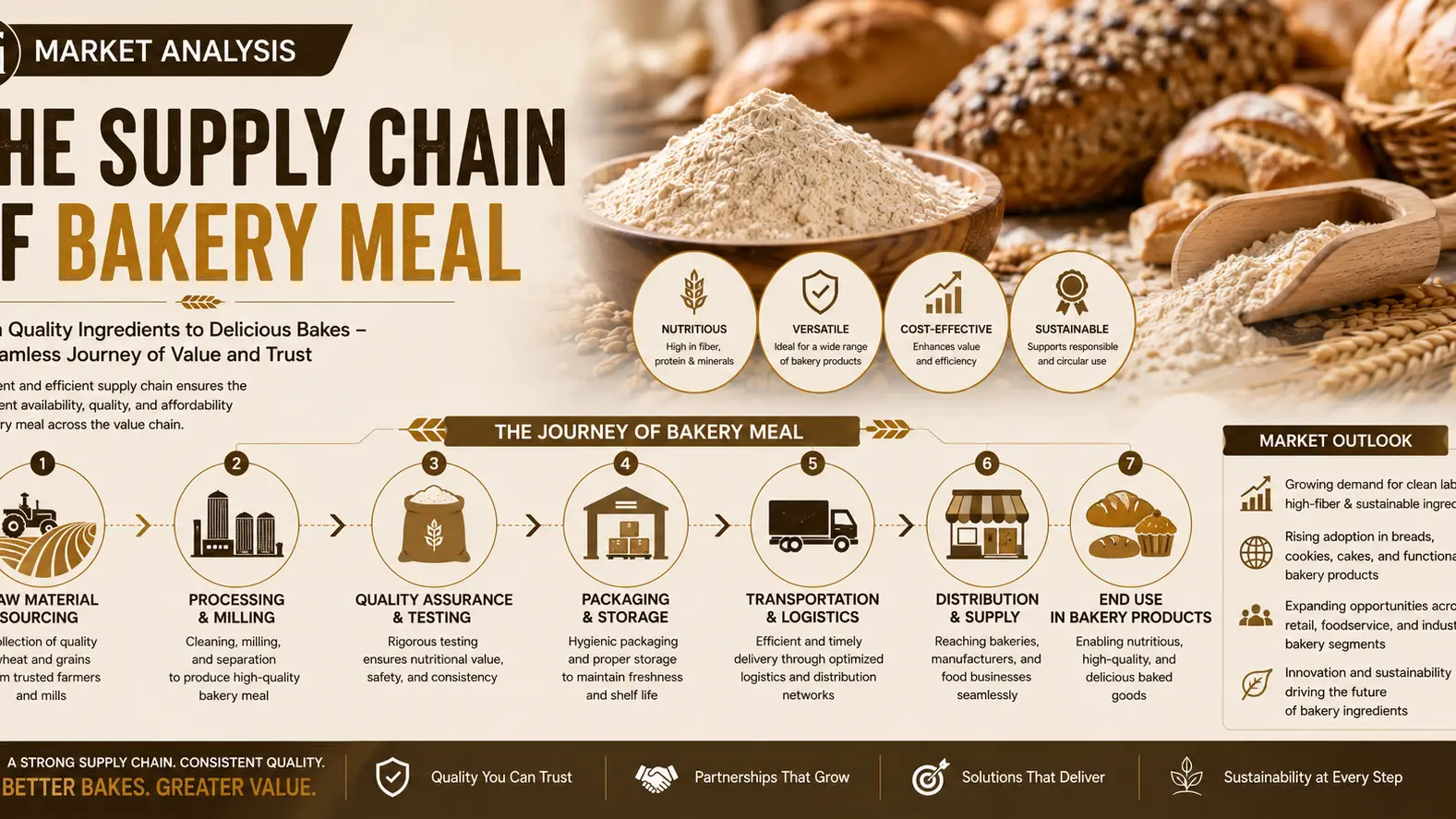

Bakery meal has emerged as an increasingly valuable platform feed ingredient within the global animal nutrition sector, supported by the growing emphasis on food waste recovery and cost-efficient livestock production. Produced from surplus bread, biscuits, cereals, and other baked goods, bakery meal offers high-energy nutritional value for poultry, swine, and cattle feed formulations. By 2026, the bakery meal market continues to benefit from rising circular economy initiatives and feed manufacturers seeking alternatives to traditional corn-based inputs amid volatile grain markets. Global bakery meal production is estimated to surpass 17.5 million metric tons, while the industry is projected to expand at a CAGR of 5.8% between 2024 and 2026. Average global pricing remains within USD 210–340/MT, depending on protein concentration, moisture levels, and regional logistics conditions.

Raw Material Recovery and Circular Supply Networks

One of the most significant developments shaping the bakery meal supply chain in 2026 is the expansion of organized food recovery systems. Large bakery manufacturers and retail chains across North America and Europe are increasingly partnering with feed processors to redirect unsold baked goods into industrial feed channels instead of landfill disposal. This model has strengthened raw material consistency while reducing disposal costs for food manufacturers. In the United States alone, recovered bakery waste volumes exceeded 6.2 million metric tons in early 2026, supporting stable feed ingredient availability despite fluctuations in grain harvests.

The integration of automated sorting and de-packaging technology has further improved operational efficiency. Modern processing facilities now achieve recovery rates above 92%, significantly lowering contamination risks and improving nutritional consistency for commercial feed applications.

Regional Production Expansion and Pricing Dynamics

Asia-Pacific has become the fastest-growing regional market for bakery meal production, particularly in China, India, and Southeast Asia, where industrial livestock farming continues to expand rapidly. European producers remain dominant in premium-grade bakery meal exports due to stricter feed safety standards and advanced recycling infrastructure.

Pricing conditions in 2026 continue to reflect transportation costs and grain substitution trends. Premium dried bakery meal with low moisture content trades near USD 330–340/MT in Western Europe, while lower-grade blended material in Southeast Asia averages approximately USD 210–240/MT. Feed producers increasingly favor bakery meal because its energy value can reduce corn inclusion rates by up to 15–20% in selected feed formulations, generating measurable cost savings for poultry and swine operations.

Logistics Pressures and Storage Optimization

Supply chain efficiency remains a central challenge for bakery meal distributors due to the product’s sensitivity to moisture and spoilage during transport. Companies are investing heavily in enclosed storage systems, pelletization technology, and regional consolidation hubs to maintain product stability across long-distance shipments.

Port congestion and container shortages observed throughout 2025 also accelerated the shift toward localized processing facilities. By mid-2026, several feed ingredient suppliers in the Middle East and Latin America adopted decentralized collection networks to shorten transportation lead times and improve inventory turnover. These logistics upgrades contributed to an estimated 11% reduction in operational losses across major bakery meal processing networks.

Sustainability Standards and Industrial Feed Demand

Sustainability reporting requirements are increasingly influencing procurement decisions among multinational feed manufacturers. Bakery meal’s ability to convert post-consumer food waste into usable livestock nutrition positions it as a strategic ingredient within low-carbon feed programs. Several feed producers now report greenhouse gas reductions of 25–30% when partially substituting conventional grains with recycled bakery meal.

At the same time, demand from poultry integrators continues to rise due to the ingredient’s digestibility and competitive energy profile. Global industrial feed demand for bakery meal is expected to exceed 14 million metric tons by the end of 2026, particularly in regions facing high corn import dependency and feed inflation pressures.

Conclusion

As a platform feed ingredient, bakery meal continues to strengthen its role within the global feed and agricultural supply chain landscape. The market’s evolution in 2026 reflects broader industry priorities centered on waste valorization, cost optimization, and sustainable livestock production. With improving recovery infrastructure, expanding regional processing capacity, and increasing industrial feed adoption, bakery meal is expected to remain a strategically important alternative feed material across international markets.

For businesses seeking stable sourcing channels, supply chain reliability, and consistent feed ingredient quality, Tradeasia International offers integrated global solutions tailored to evolving industrial requirements. Through its extensive supplier network and commodity expertise, Tradeasia International continues to support feed manufacturers and agricultural industries with dependable bakery meal sourcing across key international markets.

Sources

Leave a Comment