Zinc Sulfate Monohydrate Supply Chain Dynamics Reshaping Industrial Trade 2026

Introduction to Zinc Sulfate Monohydrate Market

Zinc sulfate monohydrate has emerged as a strategically important platform chemical in 2026, supported by its expanding role across agriculture, pharmaceuticals, water treatment, and battery precursor processing. The compound is widely utilized as a micronutrient fertilizer additive, feed supplement, and industrial intermediate due to its high zinc purity and strong solubility profile. As global food security initiatives and battery material investments accelerate, the zinc sulfate monohydrate supply chain is becoming increasingly interconnected with mining, metal refining, and specialty chemical processing industries.

The global zinc sulfate monohydrate market is projected to grow at a CAGR of 5.8% through 2030, while average international pricing ranges between USD 780–1,020/MT depending on purity grade and origin. Worldwide production volumes surpassed 1.45 million metric tons in 2025, with Asia-Pacific accounting for more than 58% of total output.

Raw Material Availability and Smelter Integration

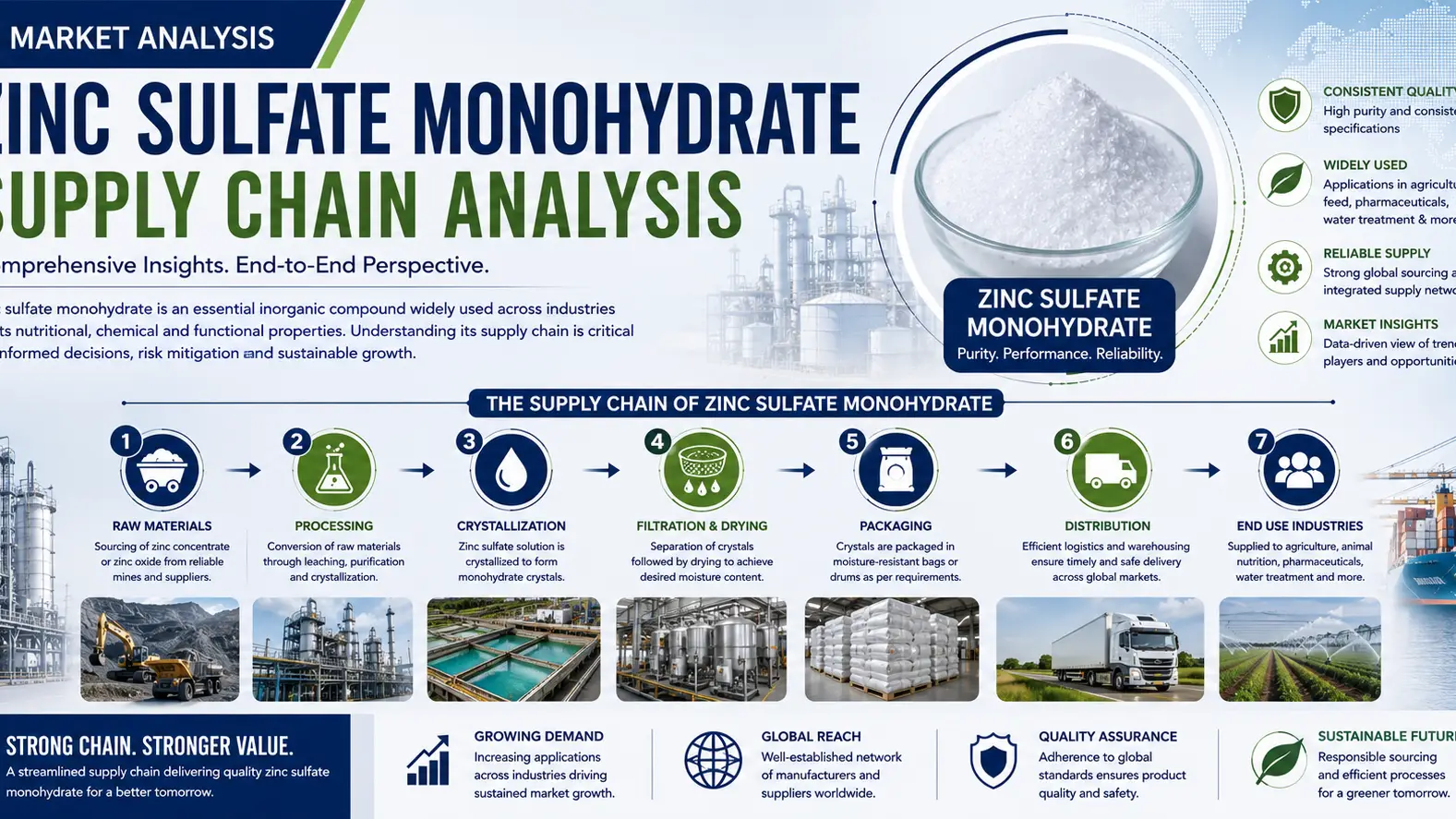

The supply chain begins with zinc concentrate mining and electrolytic zinc smelting operations, making raw material availability highly dependent on global zinc metal production. China, Peru, and Australia remain critical suppliers of zinc ore feedstock, while integrated smelter-chemical producers continue to strengthen vertical supply reliability. In 2026, sulfuric acid availability also plays a decisive role because it represents a core reagent in zinc sulfate synthesis.

Manufacturers with captive smelting assets are achieving operating cost advantages of nearly 12–15% compared with standalone chemical processors. This integration trend has become particularly important as zinc concentrate treatment charges fluctuate amid tightening ore availability and stricter environmental regulations across Asia.

Regional Manufacturing Expansion and Export Flows

Asia-Pacific continues to dominate global production, led by China and India, where industrial chemical clusters provide economies of scale and competitive export logistics. China alone contributes over 620,000 MT annually, while India’s production capacity has crossed 180,000 MT in 2026 due to rising fertilizer sector demand.

Meanwhile, North American and European buyers are increasingly diversifying sourcing channels to reduce dependence on single-origin procurement. This has encouraged new contract manufacturing partnerships in Southeast Asia and the Middle East. Export-oriented suppliers are also investing in bulk packaging systems and port-side warehousing to improve lead-time performance amid evolving global trade patterns.

Freight Costs, Energy Inflation, and Pricing Pressure

Energy-intensive refining and drying operations continue to expose producers to volatility in electricity and natural gas pricing. In early 2026, average manufacturing conversion costs increased by approximately 8% year-over-year, particularly in Europe where energy markets remain unstable.

Ocean freight normalization has partially reduced logistics pressure compared with the post-pandemic period, yet inland transportation and container shortages still affect shipment schedules for specialty chemical grades. Consequently, premium agricultural-grade zinc sulfate monohydrate prices in some regions temporarily exceeded USD 1,050/MT during peak planting seasons.

Downstream Demand from Agriculture and Battery Sectors

Agriculture remains the largest consumer segment, representing nearly 70% of global demand. Zinc-deficient soil conditions across India, Southeast Asia, and Africa continue driving fertilizer blending requirements. Simultaneously, emerging battery applications are creating new opportunities for ultra-high-purity zinc sulfate derivatives used in energy storage technologies.

Industrial buyers are increasingly prioritizing supply chain transparency, traceable sourcing, and consistent purity standards. This shift is encouraging producers to adopt digital inventory systems and long-term supply agreements to stabilize procurement cycles and improve customer retention.

Conclusion

As a platform chemical, zinc sulfate monohydrate is becoming more strategically linked to global agriculture resilience, industrial manufacturing, and next-generation energy applications. The 2026 market landscape reflects a supply chain under transformation, where raw material integration, regional diversification, and logistics optimization are shaping long-term competitiveness.

Companies seeking dependable sourcing, flexible logistics support, and consistent product quality are increasingly partnering with global chemical solution providers such as Tradeasia International. With its broad international distribution network and industry-focused procurement capabilities, the company continues to support manufacturers and industrial buyers navigating the evolving zinc sulfate monohydrate market.

Sources

Leave a Comment