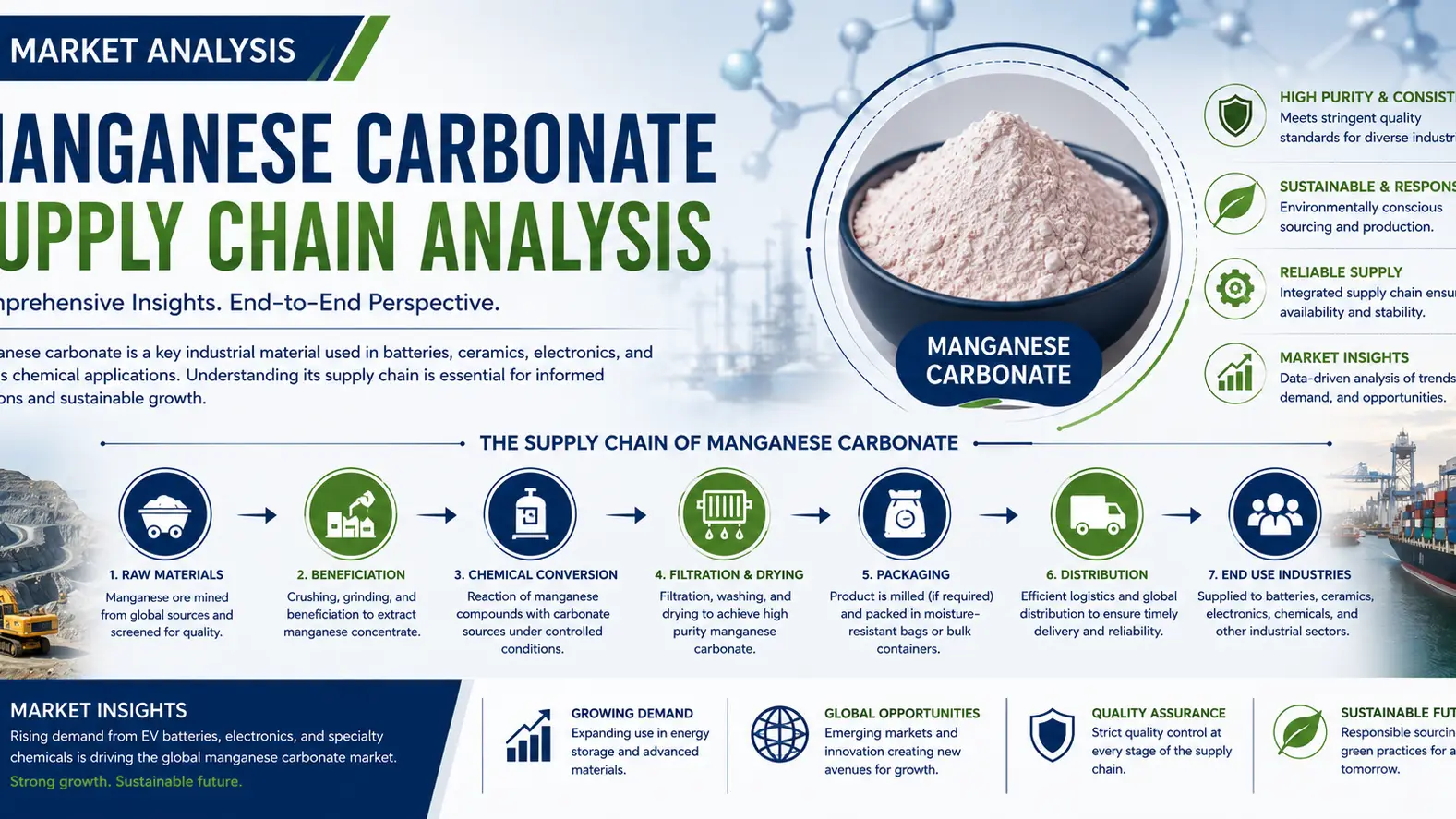

Supply Chain Transformation in the Manganese Carbonate Market

Introduction to Manganese Carbonate as a Platform Chemical

Manganese carbonate has evolved into a strategically important platform chemical within the global industrial minerals sector, supported by its expanding role in fertilizers, ceramics, pharmaceuticals, and increasingly in lithium-ion battery precursor manufacturing. By 2026, the market is being reshaped not only by demand growth but also by the restructuring of supply chains aimed at securing raw material stability and reducing exposure to geopolitical risks. Global manganese carbonate demand is projected to grow at a CAGR of 5.9% through 2030, while worldwide production capacity is estimated to exceed 620,000 MT in 2026. Market participants are closely monitoring mining output, refining bottlenecks, and transportation economics as pricing fluctuates between USD 780–1,150/MT depending on purity grades and downstream applications.

Raw Material Availability and Mining Integration

The manganese carbonate supply chain begins with manganese ore extraction, primarily concentrated in South Africa, Gabon, Australia, and China. In 2026, ore availability remains relatively balanced, although beneficiation costs continue rising due to stricter environmental compliance and energy inflation. Chinese processors are increasingly securing long-term mining stakes in African regions to stabilize feedstock procurement and reduce exposure to spot market volatility. This vertical integration trend has become essential as high-purity manganese carbonate production requires consistent ore grades above 30% Mn content. Mining and ore upgrading costs now account for nearly 38% of the total production expenditure across the supply chain.

Refining Capacity Expansion in Asia-Pacific

Asia-Pacific continues to dominate manganese carbonate refining activities, with China controlling nearly 68% of global processing output in 2026. New refining investments across Indonesia and India are gradually diversifying regional supply capabilities, especially for battery-grade manganese carbonate used in EV cathode materials. Production economics remain heavily dependent on sulfuric acid availability, energy pricing, and wastewater treatment infrastructure. Battery-grade manganese carbonate prices have climbed toward USD 1,150/MT, while industrial-grade material trades closer to USD 820/MT due to purity differentiation. Several producers are also modernizing hydrometallurgical processes to improve recovery efficiency above 92%.

Logistics Costs and Global Trade Movements

Freight volatility continues to influence manganese carbonate profitability in 2026, particularly for exporters serving European and North American markets. Bulk chemical shipping rates from Asia increased by nearly 14% year-on-year during early 2026 due to fuel adjustments and tighter maritime emissions regulations. Supply chain operators are responding by establishing regional storage hubs near major battery manufacturing corridors. Meanwhile, port congestion in select Asian terminals has encouraged buyers to diversify sourcing contracts across multiple regions. Contract structures are shifting toward quarterly pricing mechanisms instead of annual agreements, helping manufacturers better manage cost swings tied to transportation and ore procurement.

Battery Sector Demand Reshaping Procurement Models

The global electric vehicle industry has significantly altered manganese carbonate purchasing behavior. Demand from lithium manganese iron phosphate (LMFP) and nickel manganese cobalt (NMC) battery chemistries is expected to consume over 210,000 MT of manganese carbonate equivalent in 2026 alone. This transition is encouraging battery manufacturers to prioritize traceability, ESG compliance, and supply security when selecting suppliers. Strategic stockpiling agreements and multi-year procurement contracts are becoming increasingly common among cathode manufacturers in China, South Korea, and Europe. As battery applications expand, specialty chemical producers are also investing in purification technologies capable of achieving ultra-low impurity levels below 100 ppm.

Conclusion

As manganese carbonate strengthens its position as a critical platform chemical for both traditional industries and next-generation battery technologies, supply chain resilience has become a defining competitive factor in 2026. From mining integration and refining modernization to logistics optimization and battery-sector procurement strategies, the market is entering a phase where operational flexibility and reliable sourcing partnerships are essential for long-term growth.

In this evolving environment, companies increasingly seek dependable global suppliers capable of supporting consistent quality, diversified sourcing, and international distribution efficiency. Tradeasia International continues to expand its role as a strategic solution provider for industrial chemicals and raw materials, helping manufacturers navigate changing market dynamics with integrated supply chain support across multiple regions.

Sources

Leave a Comment